Neil Taylor, product design, and Peter Altero, chief business development officer, speak with Karl Loomes about fragmentation risk, margin efficiency, and the role of post-trade infrastructure as clearing expands in the US Treasury and repo markets

As more CCPs enter US Treasury clearing, is liquidity at risk of becoming fragmented — and what does that mean in practice for repo markets?

Neil Taylor: As new clearing houses enter the US Treasury (UST) clearing space, one implication is that firms may have to post margin across multiple central counterparties (CCPs) without being able to net transactions, which creates what is commonly referred to as collateral drag.

That links to what is more widely known as the CCP basis, where premiums can emerge for certain transactions or CCPs depending on netting obligations or cross-margining capabilities. Fragmentation could therefore increase capital costs for organisations because positions cannot be cross-netted across CCPs.

Peter Altero: We have seen similar fragmentation play out in other asset classes. Often, the price to clear and the cost to clear are not immediately visible. Early on, pricing between bilateral and cleared trades may appear consistent, but over time a basis can develop.

If you look back at the swaps market, there was even a basis between different clearing houses which shifted buy side market share over a period of time. I am not saying this will happen in the UST market, but it is one to watch over time post mandate. What is interesting is which other CCPs might get involved. As more products become centrally cleared, firms will likely expand their requirements of the global CCPs to support broader product coverage, or will push for inter CCP partnerships to assist clients in recognising cross-margining benefits.

Can post-trade technology genuinely prevent repo markets from becoming siloed as clearing options multiply, or is some fragmentation inevitable?

Altero: In short, yes, but the starting point for the UST market is different to what I’ve observed in other asset classes. In swaps for instance, there was already a push to electronically confirm transactions in the early 2000s which created a central authoritative data record, eliminating silos and fragmentation.

As regulators rolled out sweeping changes to the swaps market and introduced a clearing mandate, it was accompanied by a trading mandate which centralised liquidity on swap execution facilities (SEFs) and multilateral trading facilities (MTFs) and drove the majority of dealer-to-client voice transactions onto electronic venues. Technology played a pivotal role in helping customers comply with regulation, simultaneously linking a wider market segment that included their execution venues, clearing houses, and counterparties. This allowed clients to decide where to execute and clear based on pricing and liquidity, rather than technology constraints.

In repo, the objective is similar. Firms should be able to process trades in a familiar way, receive consistent messages into their risk systems, and then clear at the CCP that best suits their business. Evolution in post-trade technology is imperative to ensure a smooth transition and will also help firms drive standardisation in their workflows, especially as new clearing models, and CCPs are adopted.

Taylor: Standardisation is the critical component. When you have standardisation and a central point for transactions, many of the fragmentation issues firms experience — or may experience in the future — can be significantly reduced.

What role can portfolio optimisation, netting, or compression play in offsetting higher margin costs across multiple clearing venues?

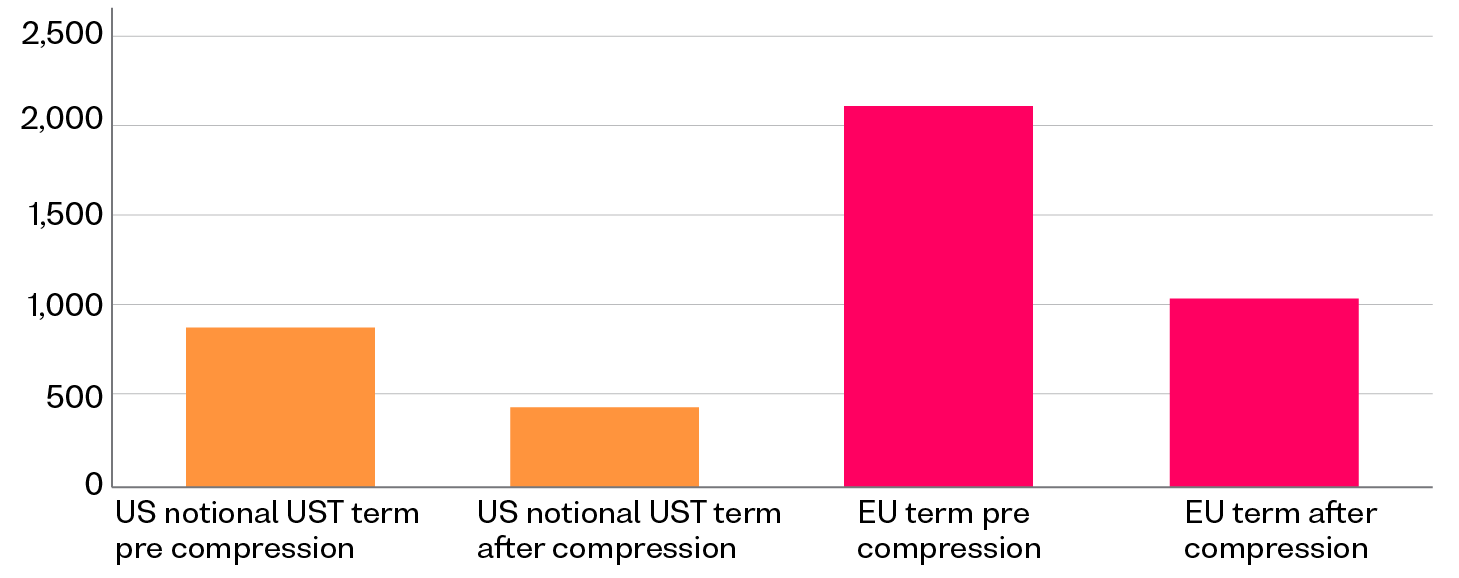

Taylor: They will play an important role. Historically, these services have not been widely used in repo, however we have seen how effective these services have been in other asset classes through OSTTRA triBalance and triReduce, and there is an opportunity to introduce similar concepts into repo.

Extensive participation in the evolution of the trading landscape in other asset classes has demonstrated our ability to help clients optimise their exposures within, and across, separate trading venues. This will allow clients and end users to retain flexibility on their choice of clearing venues. We are already developing the extension of our existing services with clients to enable more efficient use of their own financial resources (margin, balance sheet, and liquidity) in cleared and uncleared repo.

Altero: Over my 18 years in the industry, optimisation and compression have evolved significantly. Early on, when trading was largely bilateral, the primary objective was balance sheet relief. As markets moved towards clearing, optimisation providers became more important.

A common CCP and increased portfolio fungibility allowed providers to enhance their offerings and deliver better outcomes. If repo follows a similar trajectory, optimisation will grow in importance, but it needs time. Clearing is the first hurdle. The next phase — product evolution — will be the most interesting.

Repo has traditionally been flexible and relationship-driven. Is increased clearing pushing the market toward over-standardisation?

Altero: I do not think so. Firms will still be able to achieve the trade outcomes they want. There may be pressure, particularly from the buy side, to trade more vanilla products in order to access clearing benefits.

That said, repo is a deep and liquid market, and relationships still matter. If firms want to trade bespoke transactions bilaterally, they will continue to do so. Any move toward standardisation will be driven by the industry itself.

Taylor: CCPs will also evolve, offering a broader range of transaction types — such as open or evergreen repo — so that more trades can be cleared. There will always be a balance between flexibility and balance sheet relief, and CCPs will adapt because demand for flexibility remains.

OSTTRA often refers to the idea of a ‘golden trade record’. How close are firms to having a single, reliable view of their global repo positions?

Altero: I would say the industry is still not there yet, but the concept is well understood. Repo post-trade processing remains highly inefficient. Firms rely on multiple point-to-point data sources — e-mails, chats, CSV and reports from execution venues, CCPs, Prime Brokers, and futures commission merchants (FCMs) — and then stitch together multiple data formats simply to understand their position.

A central authoritative trade record in repo which is kept up to date when lifecycle events such as re rates and allocations take place, would eliminate much of the operational risk and complexity of supporting this market and its evolution.

The next step is extending that record into settlement — enabling cash flow matching, independent marks, and greater lifecycle automation to reduce settlement friction.

Taylor: Repo appears simple on the surface, but it is operationally complex, with many lifecycle touchpoints. Missed re-rates or incorrect interest calculations as an example can quickly lead to settlement failures. A central golden record removes many of those issues. It works in rates and derivatives, and there is no reason it cannot work in repo.

With T+1 now live in cash markets, how well positioned is the repo market — and is near real-time affirmation becoming essential?

Altero: It is less about mandatory affirmation and more about flexibility. Electronic trades may already be matched, but the real opportunity lies in standardised data, lifecycle automation, and settlement workflows — including predictive analytics, cash flow matching, portfolio reconciliation, and exception management to catch settlement breaks in advance of settlement date. That is how firms move closer to effective T+1 compliance and avoid potential fail penalties. Central data and affirmation workflows is a model to achieve this, but it is not the only answer.

If you could change one aspect of the global post-trade infrastructure to improve repo clearing efficiency, what would it be?

Altero: Standardisation and centralisation. If the repo market already consisted of centralised authoritative data a shift into clearing would be far easier. The market remains fragmented, and firms ultimately need to decide how much they want to invest their technology budgets as they approach regulatory changes in this market.

From a vendor perspective, that means partnering with existing platforms and acting as connective tissue across the ecosystem. We are encouraged by the constructive feedback from our key clients, which is helping us sharpen our focus on these industry partnerships.

Taylor: Post-trade repo remains under-invested in. Firms should look at what has worked in rates and credit derivatives and apply those lessons. Both cleared and non-cleared repo will remain significant, so solutions need to work across both.

This article was originally published by Securities Finance Times.