|

IN THE NEWS

|

|

Awards

|

|

We are delighted to have won the following awards in H2 this year:

Asia Risk Awards

- Portfolio Optimisation Solution.

GlobalCapital

- Americas Optimisation Service of the Year

|

➜ Read more

|

|

|

Innovation in compression – our Trade Refactoring methodology unlocks additional Rates compression potential

|

| The increased adoption of Trade Refactoring, the most sophisticated methodology for portfolio compression, has resulted in an additional USD 1 trillion of previously unavailable notional compression. A timely achievement as we enter Q4 when global banking institutions focus on reducing their gross exposures. |

➜ Read press release

|

|

|

How Trade Refactoring helps keep your interest rate portfolio leaner than ever

|

| In the last few months we have seen an increase in the adoption of Trade Refactoring which has enabled us to unlock additional benefits for compression participants. Find out how it can help your business. |

➜ Learn more

|

|

|

USD LIBOR Cessation: 2021 blueprint paves the way but requires actions now

|

| With LIBOR transition now in full swing, the focus is squarely on the upcoming USD LIBOR cessation deadline in mid-2023. How did post-trade market infrastructure adapt to support firms as they navigated the 2021 RFR transition and what’s to come in 2023. |

➜ Read article

|

|

|

Preparing for further index cessation

|

| Ready yourself for USD Libor cessation at the end of June next year. |

➜ View timeline

|

|

|

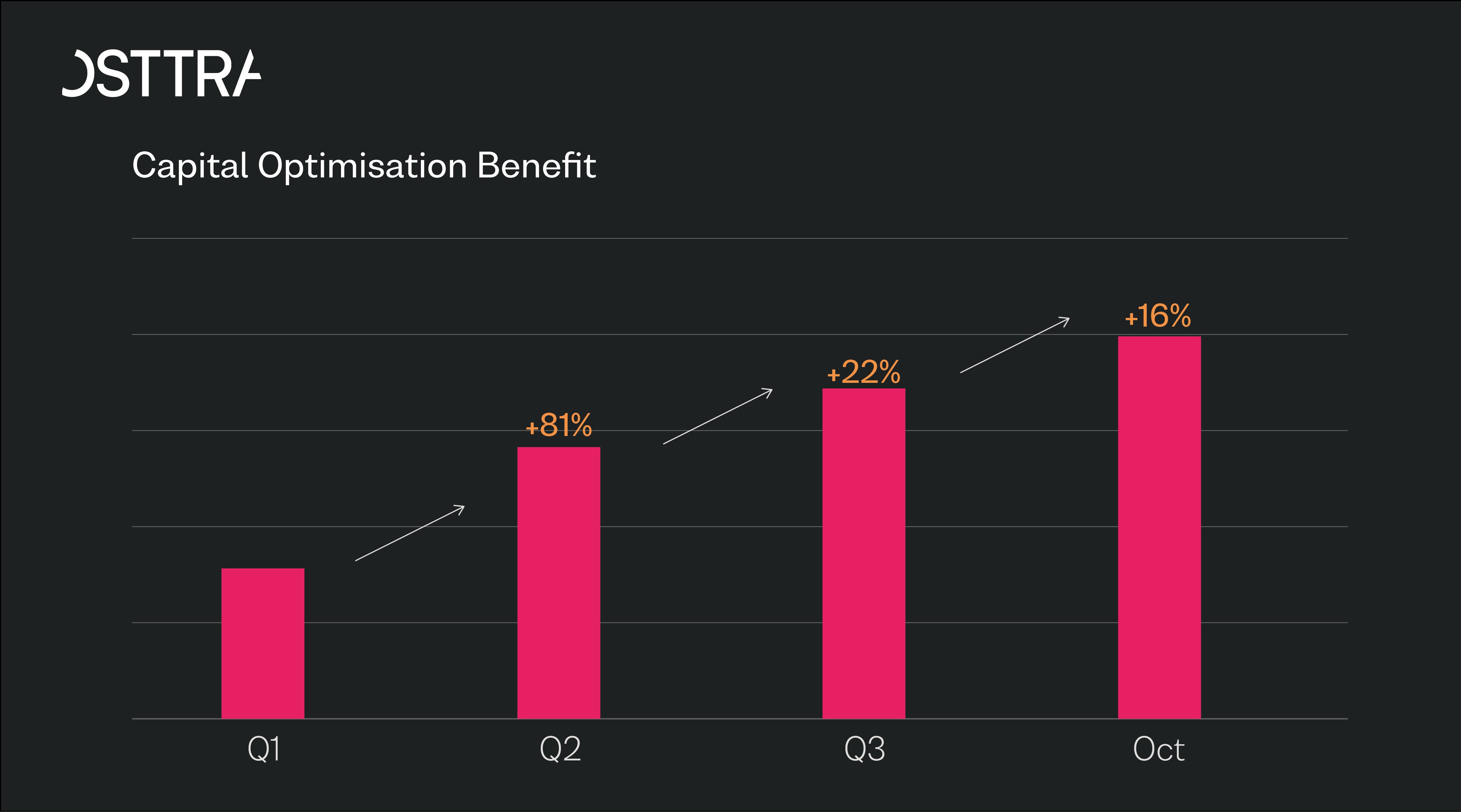

Combined credit optimisation and compression drives major capital & IM funding benefits for banks

|

| OSTTRA triBalance delivered 40% initial margin optimisation saving for credit, while OSTTRA triReduce eliminated $21.5bn of gross notional value from CMBX Index Mortgage-Backed Securities (MBS). The combined strength of both services enabled banks such as Goldman Sachs and Citi to optimise their notional, initial margin (IM) and capital exposures on a multilateral basis. |

➜ Read article

|

|

|

Supporting the market in times of market stress – Ukraine crisis

|

| This year we have seen very significant market stress in relation to settlement of RUB trades. Counterparty settlement risk has been further amplified as a result of extreme market volatility and basis risk. To help the market reduce risk we have run five RUB FX settlement risk reduction cycles, five USD/RUB cross-currency compression cycles and two single name credit cycles . Each cycle has materially reduced the settlement exposure between participants, and contributed to a reduced stress level for the market as a whole. |

➜ Contact us

|

|

|

LatAm currencies

|

We’ve completed record breaking LatAm cycles:

- Chilean peso: compression cycle at CME that was over 60% larger than our previous record

- Colombian peso: Our annual cycle at CME reduced COP465 trillion (17% of outstanding COP notional)

- Brazilian Real: Largest BRL at CME since 2020 as the network continues to expand

|

➜ Read more

|

|

|

APAC currencies

|

| Customers are joining our cycles to reduce their exposure to legacy benchmarks. Our Thai Baht non – deliverable cycles compressed 40% of the LCH outstanding notional in THBFIX – ready for the transition to the new Thai RFR, THOR. |

➜ Read more

|

|

|

GFMA engages OSTTRA for FX Close-out platform

|

| The Global Financial Markets Association’s (GFMA) FX division plans to launch a central close-out platform for FX transactions, to be used as a fall-back facility in the case of market disruption events in specific currencies. The GFMA has selected OSTTRA, powered by TriOptima, as the service provider, including reconciliation of transactions submitted by market participants, calculation of present values, and administration of the close-out agreements. |

➜ Contact us

|